Energy Transition Increases Mineral Importance

The energy transition creates a unique opportunity for Africa to move from raw material supplier to strategic industrial actor. As the importance of minerals rises proportionally with growth in the green economy, resource ownership serves only as a door opener, rather than strategic leverage. The global impetus to mitigate climate change is driving demand for critical minerals, and Africa, with significant proven reserves, is poised to transform from a raw material exporter to major industrial power. Yet the growing importance of minerals is also intensifying geopolitical competition around access, control and security.

Africa Risks Remaining Stuck in an Extractive Position.

The strategic importance of critical minerals is increasingly reshaping external engagement across parts of Africa. In regions such as the eastern DRC, competition over access to mineral resources collides with local conflict, regional rivalries and wider geopolitical interests. In such environments, external priorities can become heavily concentrated on securing resource access, often reinforcing fractured engagement rather than supporting long-term regional stability or industrial development.

At the same time, external powers increasingly pursue bilateral investment, infrastructure and security agreements with individual African states. While such arrangements may generate short-term national benefits, they can also reinforce fragmented engagement, diminish collective bargaining capacity and complicate efforts towards regional industrial cooperation.

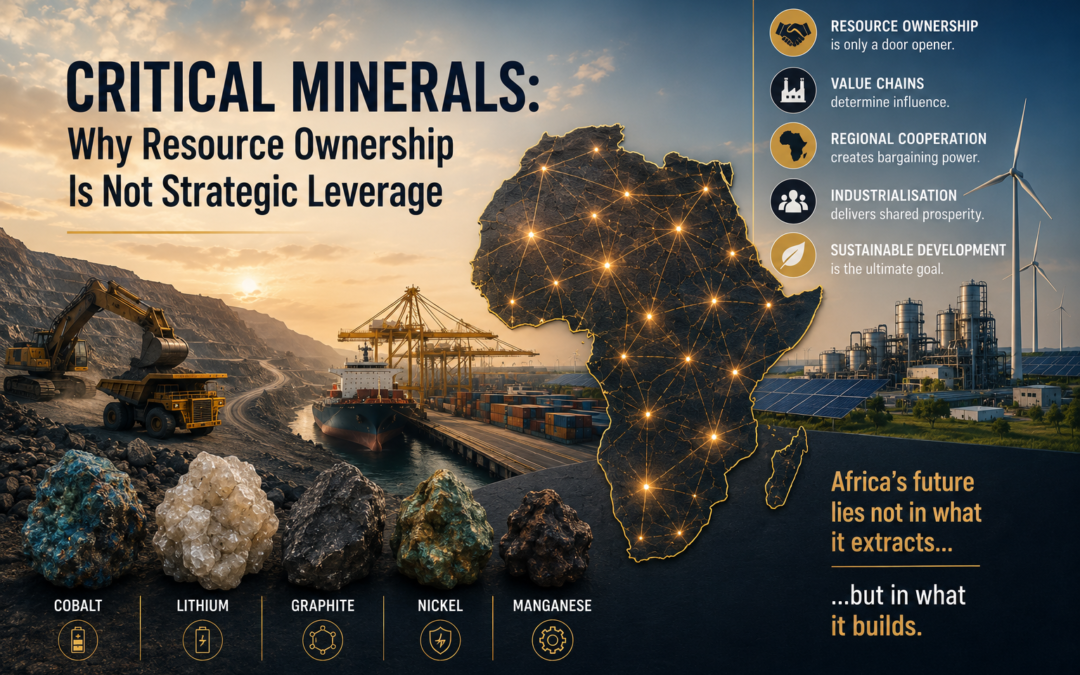

Resource Ownership is Not Strategic Leverage

In an increasingly transactional world, resource endowments alone do not translate into influence. Control over critical minerals is a major battleground for strategic competition. As African countries strive to industrialize their mineral sectors, their strength lies in collective regional negotiation. As articulated in the African Green Minerals Strategy (AMGS), Africa has a rare opportunity to harness its extensive mineral wealth. This window offers broad-based sustainable growth and socio-economic development, to industrialise and prioritise continental needs and critically, ‘to break the pattern of mineral value chains that terminate at the export of raw materials.’

Value Chains Determine Influence

Moving beyond raw material export will require sustained investment in domestic and regional processing capacity. Several African governments, including those in the DRC, Zimbabwe and Namibia have introduced tighter export controls on raw ores to encourage beneficiation and local industrial development. Similar approaches are emerging elsewhere across the continent, reflecting a broader recognition that long-term influence depends less on extraction volumes than on participation across higher-value stages of the supply chain.

Control over higher-value stages of the supply chain does not emerge in isolation. It depends on functioning value chains with ports capable of handling increased industrial throughput, cross-border transport corridors linking inland mineral production to processing hubs, stable energy supply for refining operations and regional industrial ecosystems that reduce duplication while enabling scale. It is this transformation that will determine whether Africa participates meaningfully in global clean-energy value chains or remains primarily an exporter of raw materials. In that sense, regional industrialisation is not simply a policy ambition, but a systems challenge requiring long-term alignment across infrastructure, logistics, energy and trade.

The infrastructure required to support mineral processing and higher-value regional supply chains, including transport corridors, energy systems, ports and industrial processing capacity is highly capital intensive. Without careful structuring, industrialisation financed primarily through external capital risks reproducing new forms of dependency unless African states can align infrastructure development with long-term regional continental industrial priorities.

AfCFTA and Regional Industrialisation

AfCFTA as a structural enabler of regional value chains could transform Africa’s significant resources into real influence. Greater alignment between national policy, industrial strategy and regional integration would strengthen Africa’s bargaining position within global supply chains. Without regional alignment, Africa risks repeating extractive dependency that would be carried into the future with progression of the energy transition. With it, there can be a shift from raw material exporter to high-value industrial processor, leveraging its share of global cobalt lithium, graphite and other critical mineral reserves. AfCFTA could provide the institutional framework for regional value chains, allowing African states to align trade policy, expand processing capacity and capture greater value from critical mineral supply chains. Backed by the broader institutional vision of the AU and Agenda 2063, such alignment could strengthen Africa’s position within global clean energy supply chains.

These efforts will also require structural reforms at the national level to nurture domestic processing and manufacturing capacity. At the same time, industrialisation linked to the energy transition will require investment in education, technical capability and green skills development to address shortages in expertise and prepare younger populations for participation in emerging green industrial sectors.

Challenges and Drivers

Political will to overcome competition between states and unite fragmented mineral markets for larger-scale operations is essential. Building regional value chains that harness both raw and processed mineral inputs, leveraging the diversity of critical minerals dispersed across the region requires concerted effort. African nations are accelerating midstream critical mineral processing (beneficiation) to move beyond raw material export, aiming to capture higher value in battery and green technology supply chains. Key initiatives include limiting raw exports, developing regional refining hubs, and investing in refining plants for lithium, cobalt, and copper in countries like Zimbabwe, the DRC, and Morocco.

The race for supply security from the US, EU, China and other external partners is reshaping investments, aiming to balance national security with African industrialization. Successful midstream expansion requires substantial investment in energy and logistics. Adoption of best practice – whether it is from a democratically elected government or a government whose legitimacy is contested – by regional institutions such as the AU through the vehicle of AfCFTA presents the best posture for regional alignment. Regional industrialisation will depend not only on mineral reserves, but on the ability of African states to coordinate infrastructure, trade and policy over time.

Coordination transcends simple alignment on interests. A major constraint is that, unlike the EU, the AU is not a supranational body. Therefore, it lacks the legal authority to negotiate trade deals on behalf of member states; this constrains collective bargaining with trade partners. Furthermore, existing institutional frameworks, including AfCFTA, were not conceived as geopolitical instruments. Their evolution will inevitably be gradual. But the speed of global change is accelerating. The question therefore is not about evolving frameworks, but Africa’s capacity for coherence, harmonisation and alignment amid transformation. Africa’s advantage is real. Converting it into leverage will depend less on ownership, and more on scaling those assets into strategic and industrial power.

External Competition and Industrial Priorities

The challenge for African states is not to resist external interest, but to structure it in ways that support long-term industrial development and value creation before external competition reproduces extractive dependency within the energy transition.

The energy transition will reshape patterns of industrial power over the coming decades. Whether Africa remains primarily as a raw materials exporter or emerges as a meaningful participant across higher-value industrial systems will depend less on ownership, and more on the continent’s ability to translate scale, infrastructure and regional integration into long-term productive capacity.